Understanding Proof of Loss Declarations

If you are going through the process of filing a home insurance claim in the Los Angeles area, you are probably already aware of the overwhelming amount of paperwork involved. Whether the claim relates to water damage, fire damage or theft, you will probably be required to submit a sworn loss declaration before you are able to receive your settlement payment. As claims adjusters, we deal with this kind of paperwork all the time, so we can help explain the purpose of this document as well as offer some guidance as to how to fill it out properly.

What is a loss declaration?

When it comes to homeowner’s insurance, the burden of proof falls upon the insured party. This means that your insurance provider requires you to present evidence of your loss in the event of an accident that leads to a claim.

Therefore, the proof of loss declaration serves as an official, notarized, and sworn statement to your provider explaining the degree of property damage you have suffered from the accident as well as the total monetary value of the destroyed or damaged property. This document is usually one page and offers a summary of the important information you are required to provide based on your policy.

Your insurance company uses this information in order to determine the extent of their obligation to you for the property loss you have suffered. Once the document has been submitted, they will review your claim and respond with their own assessment of the matter.

Is there a difference between total loss declarations and proof of loss declarations?

Both ‘proof of loss declaration’ and ‘total loss declaration’ are used interchangeably to refer to the document we have explained above. Don’t let the two different terms confuse you. They both refer to the sworn proof of loss statement you will need to submit when filing your homeowner’s insurance claim.

When do I submit my proof of loss declaration?

Submitting your proof of loss declaration happens early in the process of filing your claim. Many insurance providers have a standardized document that you need to receive from them, complete, and have notarized.

Most insurance policies require that you complete and submit this document within 60 days, so the best course of action is to take care of it as quickly as possible. You should explicitly discuss the deadline with your provider and request an extension if you don’t believe you will be able to submit it on time.

What do I need to include in the declaration?

The first step in completing a proof of loss declaration is to review your insurance policy because it contains certain details you will need to include on the form. Most proof of loss declarations require you to provide the following:

- Date and time of the accident

- Whether the home was occupied at the time of the accident

- Ownership and title information for the property

- Total amount of coverage available under your insurance policy

- The estimated actual cash value of the damaged property

- Total value of the loss

- Total amount you are claiming under your policy

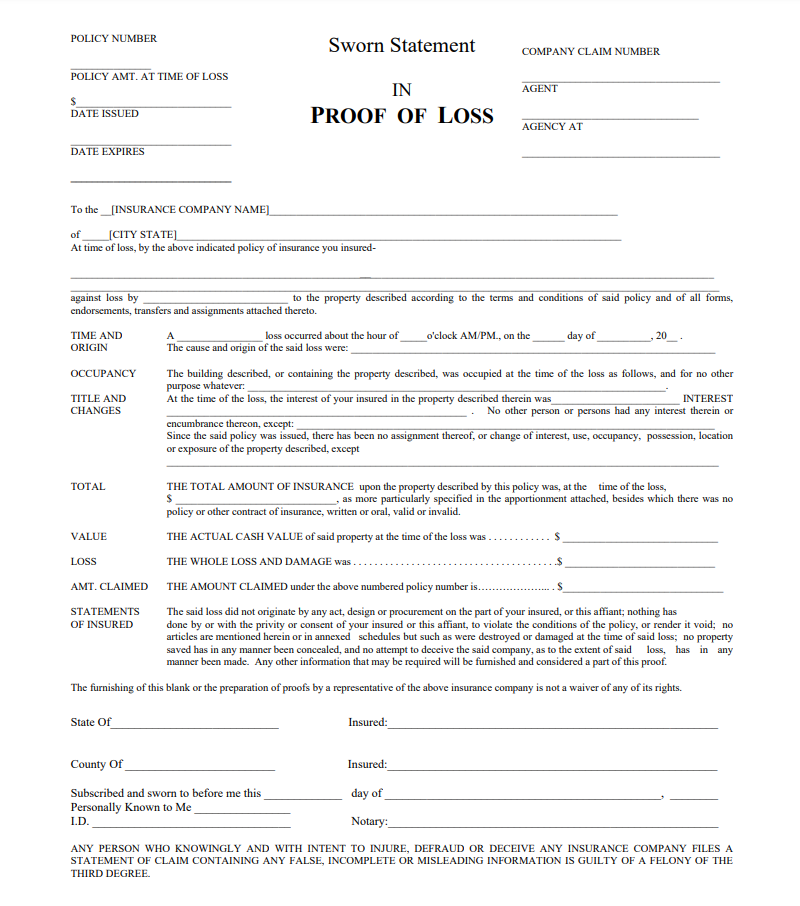

We have provided an example of a proof of loss declaration form below for illustration purposes. You’ll notice that in addition to the information mentioned above, the form includes a ‘Statement of Insured’ which states you had no part in the accident.

*Please note that the document below is simply a general example and the one provided by your insurance company may differ slightly.

How do I estimate the value of damaged property?

This aspect of the proof of loss declaration is the most difficult because it requires accuracy and organization on the part of the homeowner. Insurance providers deal with homeowner’s claims on a daily basis, so it is crucial that you are as honest and accurate as possible. You must be able to provide facts and evidence to back up your estimate as misrepresenting the value of your loss can result in underpayment, delay and even denial of your claim.

The best way to determine an accurate estimate is by creating a thorough household inventory. You may have already created one upon purchasing your policy, so this is a great reference through which to gather the information you need.

We recommend purchasing a binder in order to store physical receipts and making a spreadsheet in order to stay as organized as possible. Online or paper credit and debit card statements are an excellent source of information because they provide an itemized list of your purchases as well as dates of purchase.

Here is an example of what your household inventory spreadsheet might look like. Take note of the categories we chose (Condition, Description, Cost, Area, etc.) and be sure to include as much relevant information as you can. The more information you can provide to support your estimate, the better your chances will be of receiving a fair settlement payout.

Though it requires a significant amount of time and effort, creating a comprehensive inventory of your property loss/damage is the absolute best way to substantiate the estimates you include on your proof of loss declaration. Insurance providers are far less likely to question the claims of homeowner’s who put in the necessary legwork to generate accurate estimates.

How can a public adjuster help with my proof of loss form?

As public adjusters, we deal with insurance claims on a daily basis and know how taxing the inventory process can be for those who have just been the victim of a significant accident. In addition to trying to get your life back on track and provide for the immediate needs of your family, you must also navigate the difficult world of coverage limits and insurance industry terms.

At Avner Gat, Inc., our team of dedicated public adjusters can help you complete your proof of loss declaration properly and represent your interests in dealing with your insurance provider. We have decades of experience negotiating with insurance companies on our clients’ behalf and have gained the expertise to guide you through the entire process.

Our adjusters will do everything in their power to make sure you are properly compensated for your loss and take as much of the stress off of your shoulders as we can. As public adjusters, our mission is to get you paid every dollar you are owed under your homeowner’s insurance policy.

Final Thoughts

We hope that our explanation of proof of loss declarations has given you a better understanding of what they are and what purpose they serve in the claims process. If you have recently suffered a loss as a result of an accident, do not hesitate to contact us with any questions you may have about your claim. The team at Avner Gat, Inc., would be happy to discuss your particular situation and provide you with any guidance you need during the claims process.

To speak with one of our experienced public adjusters about your claim, call us at (818) 917-5256 or fill out the contact form below and let us know how we can help you!