Home » Property Insurance Claims | Los Angeles » Water Damage Insurance Claim | Los Angeles

Water Damage Insurance Claim Los Angeles

Water damage is the second most common cause of homeowners insurance claims after wind & hail damage. According to the Insurance Information Institute, about one in 50 insured homes has a property damage claim caused by water damage each year.

Many water damage claims are relatively small and easy to manage. However, large or complex claims can be a nightmare to deal with!

This is often the case when you don’t fully understand your insurance policy and are out of your depth negotiating with an experienced insurance adjuster. And if you have time constraints and are not used to dealing with contractors, you might be in for a rough ride.

If you’ve suffered water damage to your home and are feeling frustrated and unsure on how to proceed, you’ve come to the right place.

Note: Not all homeowners insurance policies provide the same coverage. Always check your policy to see what water damage causes you’re covered for as specific requirements and limits can differ from policy to policy. If you’re unsure about anything, talk to your insurance provider or contact a licensed public adjuster for assistance.

Does Homeowners Insurance Cover Water Damage?

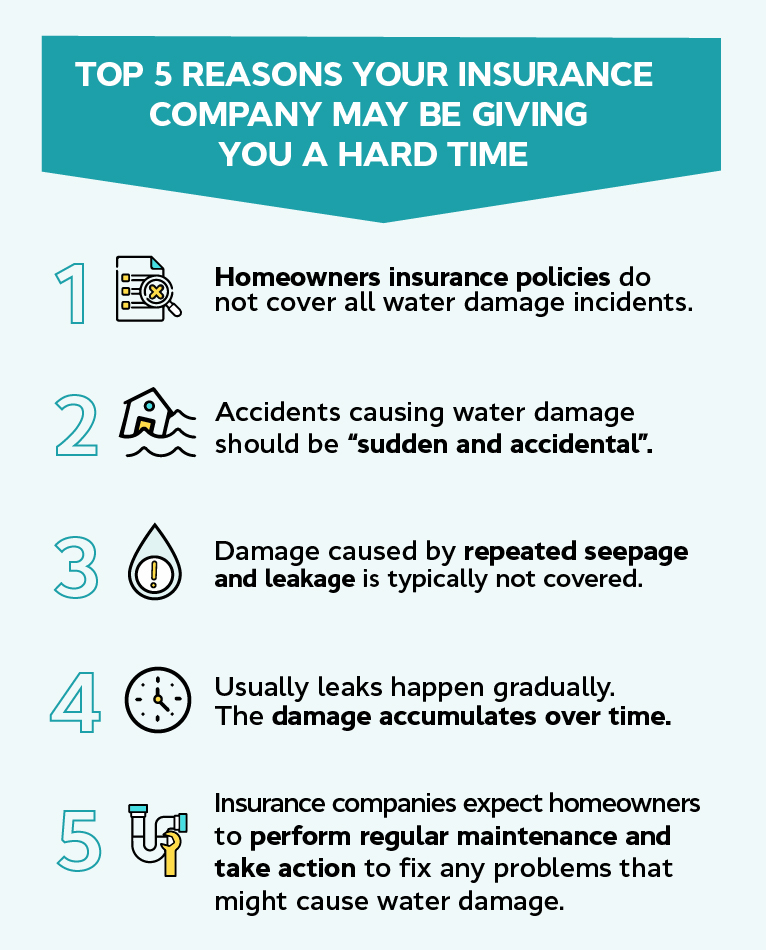

Most homeowners insurance policies will typically cover water damage if the cause is sudden and accidental. This may seem simple and straightforward, but as the saying goes, the devil is in the details.

Let’s look at two examples.

Line Breaks

Homeowners insurance policies typically cover water line breaks. However, this isn’t cast in stone such as when the water line has been leaking for a long period of time.

Most home insurance policies limit water damage coverage to water that hasn’t entered your home from the ground or sewer. Note that you can obtain sewer backup coverage from most insurance companies for an additional fee.

Mold

Mold is often a consequence of water damage. So will your homeowners insurance policy cover mold? It’s not always an easy question to answer. It typically depends on what caused the mold.

Usually, mold damage might only be covered if it can be directly linked to a covered event. But if the homeowner didn’t do anything to prevent the mold or allowed it to get worse, it’s unlikely that it will be covered.

Differentiating Between Water Damage and Flood Damage

Many homeowners think water damage includes damage caused by a flood. This is a popular misconception.

Standard homeowners insurance policies will not cover flood damage. If you want to have flood damage insurance, there are flood-specific insurance policies available on the market.

What Is Flood Damage?

The Federal Emergency Management Agency (FEMA) defines flood damage as follows:

“A general and temporary condition of partial or complete inundation of 2 or more acres of normally dry land area or of 2 or more properties (at least 1 of which is the policyholder’s property) from:

– Overflow of inland or tidal waters;

– Unusual and rapid accumulation or runoff of surface waters from any source; or

– Mudflow; or

Collapse or subsidence of land along the shore of a lake or similar body of water as a result of erosion or undermining caused by waves or currents of water exceeding anticipated cyclical levels that result in a flood as defined above.”

This definition is a good place to start if you want to assess whether your water damage will be attributed to flooding. Flooding usually occurs during natural disasters.

What Are Your Responsibilities as a Property Owner?

As a property owner, you are responsible to maintain your property and take the necessary steps to prevent or reduce the risk of water damage.

The first thing you should do when you notice a potential water damage event is to mitigate the damage. The longer an area remains wet, the higher the likelihood that damage to the area will get worse and spread to surrounding areas. You may need to hire an emergency drying service company to assist.

Note: Do not dispose of any items that have suffered water damage. Most policies require you to make the damaged items available for inspection. This allows your insurance company to more easily verify the value of damaged items.

Gradual Damage vs. Sudden and Accidental Damage

A standard homeowners insurance policy typically only covers water damage that’s caused by a sudden and accidental event.

The damage may appear to be sudden to you because it wasn’t visible at first. However, your insurance company might argue it existed before you noticed it and it became worse over time. Gradual water damage encompasses normal wear and tear.

Note that some insurance companies like American Family Insurance (AMFAM) provide optional coverage for hidden water damage. In the case of AMFAM:

“It covers the cost to repair damage done by a hidden water leak you can’t see within the walls, floors, ceilings, cabinets, beneath the floors or behind or under a home appliance.”

How Long Do You Have to File an Insurance Claim After a Water Damage Accident?

While all policies are different, most insurance companies require that prompt notice is given to the company. This means that if you have suffered water damage, you must notify your insurer or agent right away. Furthermore, you should file your claim as quickly as possible to avoid a breach of your insurance policy, which might result in your claim being denied.

Water Damage Insurance Claim Process

Once you’ve filed your water damage insurance claim, your insurance company will appoint an insurance adjuster to investigate your claim. If your claim is accepted, you’ll be provided with a settlement amount so you can hire a contractor to repair the water damage. Most policies will also cover the costs to repair or replace items in your home that suffered water damage.

Why Should You Hire a Public Adjuster for Your Water Damage Claim?

Here are some of the main reasons why it’s smart to hire a public adjuster.

Evens the Playing Field

Managing a large or complex water damage claim on your own can be challenging. There are many intricacies that you may not be aware of and it can cost you dearly. You can quickly find yourself confused and out of your depth.

A good public adjuster has the knowledge and experience to manage your homeowners insurance claim on your behalf. They always act in YOUR best interests.

Saves You Time

Dealing with a large or complicated insurance claim can be very time-consuming. It can feel like a second full-time job. Allowing a public adjuster to manage the process on your behalf will save you a lot of time. And it’s comforting to know that your claim is in good hands.

Negotiates on Your Behalf

Negotiating with the insurance adjuster who has been appointed by your insurance company can be difficult. They act in the best interests of the insurance company, not your best interests.

A reputable, licensed public adjuster that has years of experience can often negotiate a much better settlement agreement.

Works on a Contingency Basis

Public adjusters typically work on a contingency basis and their fees are solely based on a percentage of the settlement amount. This motivates them to work hard to get you the best possible deal available under your homeowners insurance policy in the shortest amount of time.

Faster Submission of Information

If you’ve suffered water damage to your home, you want your insurance claim and repairs to be finalized as soon as possible. Public adjusters deal with insurance claims daily. They know how to quickly organize and submit the correct documentation in support of your claim.

They don’t have to second guess what to do or what to do next. This can usually help to resolve your claim faster than if you were to do everything yourself.

Whether you’ve received a bad settlement offer or don’t have the time and experience to manage your claim and deal with contractors, a public adjuster can help.

Avner Gat, Inc. has 15+ years of experience as a public adjuster in Southern California. We protect homeowners from the games and fine print that insurance companies are known for.

Call Avner now at (818) 917-5256 to find out how we can assist you.